Are your customers leaving you behind digitally? If you can’t offer your customers a great digital experience (i.e., an easy-to-use website, awesome mobile experience), you are inviting great-customer-experience firms like Amazon into your marketspace. Fortunately, being better at digital business seems to help growth. We found that enterprises with above-average digital business effectiveness had revenue growth eleven percentage points higher than their industry average.[foot]MIT CISR 2010 Digital Business Models survey, N=130. Digital business effectiveness (a combination of eighteen questions) is statistically significant in a regression against revenue growth, controlling for enterprise size and industry.[/foot] This briefing looks at where to start, and shows how one company—Banco do Brasil—created a powerful digital business model.

Companies with Better Digital Business Models Have Higher Financial Performance

Abstract

At MIT CISR, we have developed a framework to help enterprises strengthen how they do business digitally with their customers via three capabilities: content (what is consumed), customer experience (how it is packaged), and platform (how it is delivered). But if your business has traditionally delivered products and services through non-digital channels, how do you develop an effective digital business model? This briefing shows how great digital business models are linked to better firm performance, looks at where to start, and shows how one company—Banco do Brasil—created a powerful digital business model.

Are your customers leaving you behind digitally?

The Three Essential Capabilities of Your Digital Business Model

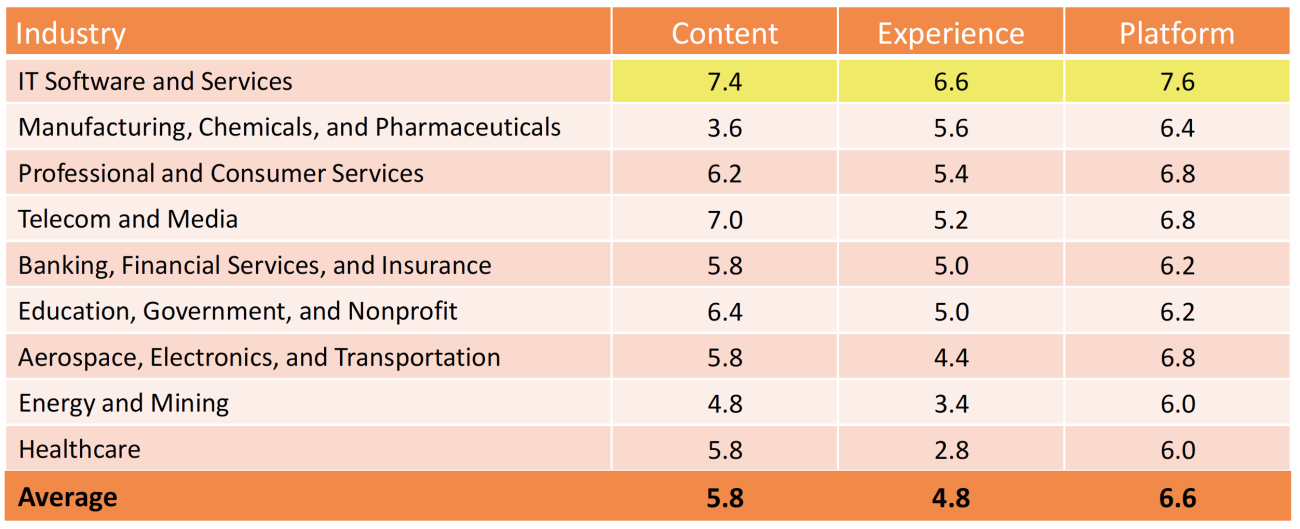

At MIT CISR, we have developed a framework to help enterprises strengthen their digital business models (i.e., how companies engage customers digitally) via three capabilities: content (what is consumed), customer experience (how it is packaged), and platform (how it is delivered). To better understand digital business models, we surveyed companies to assess the effectiveness of their content, experience, and platform (see figure 1). The industry with the strongest effectiveness scores overall (the highlighted cells in the figure table) was IT software and services, while energy and mining and healthcare were among the weakest. However, regardless of industry, top financial performers had better digital business model effectiveness. In the financial services industry, for example, the top third of financial performers had respectively 22%, 41%, and 21% better content, experience, and platform scores on a basket of growth and net margin than the bottom third of performers. This is good evidence that firms with better digital business models also have stronger financial performance.

We have studied the successful digital business models of companies like Amazon, Apple, Bloomberg, Banco do Brasil, Commonwealth Bank of Australia, DirecTV, ING Direct, Google, Netflix, and USAA, and analyzed survey results from 130 enterprises. For an industry-leading digital business model, your enterprise has to have good content, customer experience, and digital platforms.

But if your business has traditionally delivered products and services through non-digital channels, how do you develop an effective digital business model?

Where Should You Build Capabilities?

The place to start depends on your strategic goals.[foot]This section reports statistically significant regressions between effectiveness of the three components of a digital business model and different measures of firm performance. [/foot]

- If your goal is driving new digital revenue, then start with strengthening your digital content (new products and features and new product information). More new content— and the associated buzz—is correlated with revenue increases.

- If your goal is cross-selling and driving more revenue per customer, focus on improving your customer experience. A rich customer experience that includes easy-to-use interfaces and the ability to self serve and get input from fellow customers makes consumers more likely to buy more of your products.

- If your goal is profitability, then focus on building, reusing, and exploiting the shared digital platforms. Firms with better digitized platforms had better net margins.

Eventually you will need to be great in all three areas to have a world-class digital business model, but attempting to build all of these three is a daunting task. Finding the correct starting point is essential. Here is how Banco do Brasil used a strategic goal—fast growth while managing the costs of serving customers—as an entry point on its digital journey.

Figure 1: Effectiveness of Content, Experience, and Platform by Industry

Source: MIT CISR 2010 Digital Business Models Survey, N=130

Questions per capability: Content = 6; Experience = 7; Platform = 5

Highlighted cells indicate the strongest effectiveness scores for each capability

For an industry-leading digital business model, your enterprise has to have good content, customer experience, and digital platforms.

Banco do Brasil: Creating a DBM That Cuts Costs and Serves More Customers

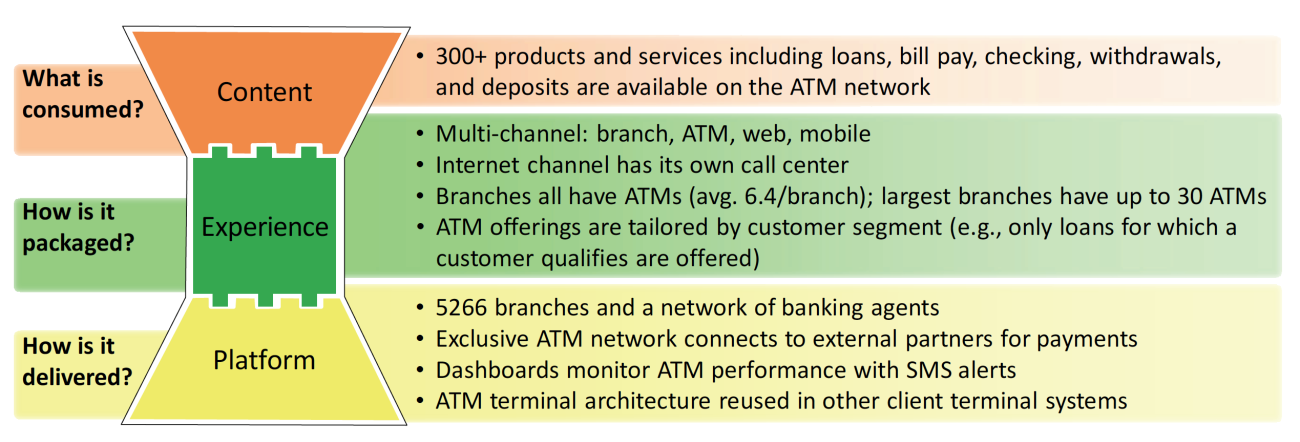

Banco do Brasil is the largest Latin American bank by assets, with over 55 million customers. Active in twenty countries, it has a 19% market share in Brazil. Customer growth was 28% from Q1 2010 to Q1 2012. Some years ago, Banco do Brasil faced an interesting dilemma. As a very successful bank with lots of products in a fast-growing part of the world, it needed a way to grow while cutting the costs of serving customers. As Internet penetration was still quite low in Brazil, Banco do Brasil decided to create a world-class network of 44,000 ATMs to address its fast growth while managing costs. These ATMs now allow its customers to access more than 300 products and services. Although the bank has more than 5,000 branches and a network of banking agents, management felt digital banking—specifically ATMs—was the right digital business model for growth. But the bank also wanted to emphasize the customer experience and make each customer feel a personal connection to increase loyalty and retention. CEO Aldemir Bendine explained, “We want to be a bank tailored to customer needs, where each one feels personally served in all our channels.”

To achieve this goal of personalization, the bank uses income, direct deposit information, investments, and age to allocate each customer to a segment. The bank’s ATMs then tailor menu selections based on the segment profile. For example, there are five segments for individual customers and five for companies, organized by income and assets. Within the segments are niches, such as university students, public servants, farmers, and military. The segment profile helps in filtering so that customers see only products attractive to them. In addition, Banco do Brasil can add behavior to the tailoring criteria (e.g., “Are you in the market for a car loan?”).

Interestingly, customers are more likely to apply for loans at the ATM because they don’t have to explain why they need one. The customer sees only the credit lines for which she or he is able to apply, and can create payment simulations of different loans. Once a loan is chosen, the customer is offered loan insurance for an extra fee, including an online health status review. When the customer confirms the information, the loan is approved and funds are immediately made available.

To help overcome reluctance to move from using tellers, most branches have greeters in the self-service ATM area. Greeters have two main roles: to help customers use the ATMs (about 10% of customers need human help) and to highlight and sell customers additional products that are available via ATM.

This successful ATM network is now being integrated and optimized for self service across multiple channels including mobile, internet, and digital TV. The results are impressive. Net income improved 5.3% per annum (2008–2012) and about 40% of personal loan applications are now made through ATMs. ATM is Banco do Brasil’s most popular channel and has the highest satisfaction rating. More than 90% of customers use ATMs and this channel accounts for 44% of the bank’s total transactions.

In order to enhance customer experience and build on its successes, Banco do Brasil is now integrating mobile channels with the ATM network. A recent innovation enables customers to apply for personal loans via cell phone. The transaction is confirmed via SMS and the loan appears immediately in the account. Customers can then access the funds electronically or as cash at an ATM. For Banco do Brasil, its digital business model focused on using ATMs both to improve customer experience and to increase efficiency (see figure 2). The ATMs allowed Banco do Brasil to customize its large set of products to customer needs and increase the bank’s margin by exploiting a digital platform—all while growing fast.

It’s Time to Start Building Your Digital Capabilities

Now is the time to review your digital business model and its link to your future performance. We have reached a tipping point and all industries need to work on their digital business models. Even industries dependent on physical interaction—like healthcare—are increasingly digitized and, given our survey results, have a lot of room for improvement!

So what to do? The three capabilities required for an effective digital business model—content, experience, and platform—build on one another. To develop strength in all three areas, you need to find your equivalent of Banco do Brasil's world-class ATM network: an entry point tied to your strategic goals. From there, your digital business model can evolve into a competitive advantage.

Figure 2: Banco do Brasil’s Digital Business Model

© 2013 MIT Sloan CISR, Weill and Woerner. CISR Research Briefings are published monthly to update MIT CISR patrons and sponsors on current research projects.

About the Authors

Peter Weill, Chairman and Senior Research Scientist, MIT Sloan Center for Information Systems Research (CISR)

Stephanie L. Woerner, Research Scientist, MIT Sloan Center for Information Systems Research (CISR)

MIT CENTER FOR INFORMATION SYSTEMS RESEARCH (CISR)

Founded in 1974 and grounded in MIT's tradition of combining academic knowledge and practical purpose, MIT CISR helps executives meet the challenge of leading increasingly digital and data-driven organizations. We work directly with digital leaders, executives, and boards to develop our insights. Our research is funded by member organizations that support our work and participate in our consortium.